Introduction

In the world of construction projects, there exists a realm of costs and activities that cannot be directly attributed to a specific measured work. These costs, known as preliminaries, play a crucial role in the successful execution of any project. Just like the foundation of a building, preliminary items provide the groundwork for smooth operations and efficient progress. So, what exactly do we mean by preliminaries in a Bill of Quantities (BOQ)? Let’s delve into this intriguing topic and uncover the key elements that make up these preliminary items.

What are Preliminaries in a BOQ?

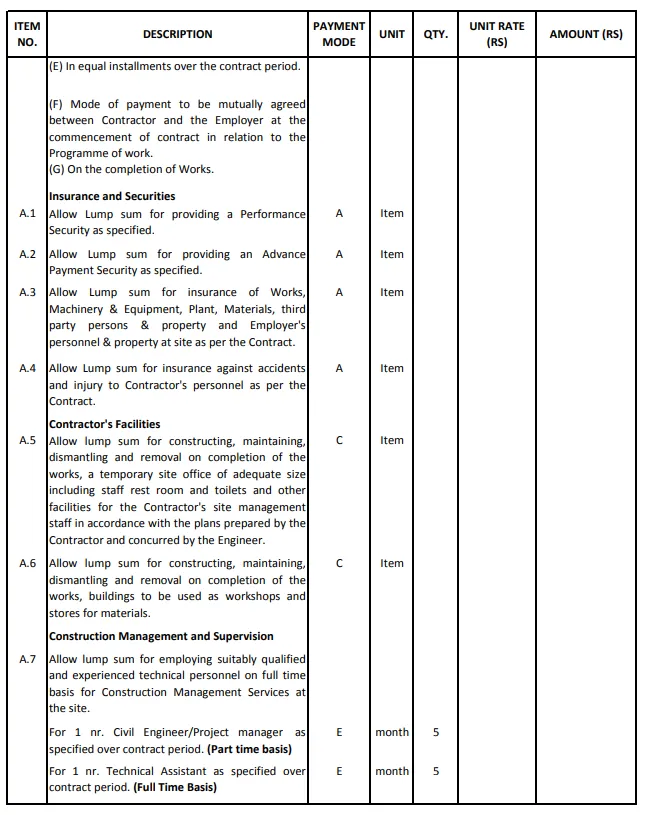

At first glance, the term “preliminaries” may seem vague and elusive. However, in the context of a BOQ, it refers to the contractor’s costs that cannot be directly allocated to a specific measured work. Instead, these costs are grouped together and listed under the Preliminary Bill section. Think of it as a hidden treasure chest containing expenses that are essential for the smooth functioning of a construction project.

One common example of preliminaries is the cost of administering a project. This includes various activities such as project management, documentation, coordination, and supervision. Additionally, preliminaries encompass the provision of general plant, site staff, facilities, site-based services, and other items that cannot be included in the unit rate of a particular measured work. For instance, the cost of a shared site office, which supports the completion of the entire project, cannot be allocated to a specific measured work. It is through these preliminary items that the intricate web of construction operations comes to life.

Now that we have a clearer understanding of what preliminaries entail, let’s explore the different categories they can be classified into and discover real-life examples for each.

Categories of Preliminaries and Their Examples

Preliminary items can be categorized into distinct groups based on their purpose and the requirements they fulfill. Let’s explore these categories one by one, accompanied by concrete examples for better comprehension.

1. Contractual Requirements

The first category of preliminary items revolves around the contractual requirements set forth in the Conditions of Contract. These requirements serve to protect the construction rights of the employer and ensure adherence to the agreed terms and conditions.

Examples of preliminary items falling under this category include bonds and guarantees, which provide financial security and assurance to the employer. Additionally, insurances play a vital role in mitigating risks and safeguarding the interests of all parties involved.

Now that we’ve uncovered the preliminary items related to contractual requirements, let’s move on to the next category: specific requirements specified by the employer.

2. Specific Requirements

In construction projects, the employer may have specific requirements that go beyond the standard contractual obligations. These requirements can vary widely, depending on the nature of the project and the expectations of the employer.

Preliminary items falling under this category include employer’s and engineer’s facilities, testing of materials, testing of works, and temporary works such as traffic diversion and temporary access roads. Furthermore, elements like project signboards and photographs serve as visual aids and documentation tools, capturing the essence of the project’s progress and milestones.

Having explored the specific requirements, let’s proceed to the next category, which revolves around the tenderer’s intended method of executing the works.

3. Method-Related Charges

Every construction project has its unique execution strategy, and preliminary items play a significant role in supporting the chosen method. This category encompasses items that are directly related to the tenderer’s intended method of executing the works.

Examples of such preliminary items include contractor’s facilities, site transport, and plants like concrete mixing plants. These items are vital for ensuring the smooth flow of construction activities and aligning with the selected method, ultimately leading to successful project completion.

Now that we have explored the categories of preliminaries based on their purpose, let’s shift our focus to another perspective: categorizing preliminary items based on the way the cost is incurred.

Categorizing Preliminary Items Based on Cost Incurrence

Beyond their purpose, preliminary items can also be categorized based on the way costs are incurred. This perspective sheds light on how these costs vary and provides insights into their nature. Let’s delve into the two primary categories of preliminary items based on cost incurrence.

1. Cost-Related Items

Under this category, preliminary items represent costs that are fixed and depend on the employer’s requirements.

Take, for example, the erection of a site office. The cost of setting up the office, including its size, type, and the facilities to be included, is predetermined. These costs remain unchanged throughout the project duration, acting as stable foundations that support the project’s administrative and operational needs.

2. Time-Related Items

In contrast to cost-related items, time-related preliminary items vary based on the duration of the project.

The maintenance of a site office is a prime example of a time-related item. As the project progresses, the site office requires ongoing maintenance and incurs running costs. The unit of measurement for such costs is typically the “month.” As the project duration extends, the maintenance costs also increase, creating a dynamic dance between time and expenses.

Now that we have gained a deeper understanding of the different ways preliminary items can be categorized, let’s explore another dimension: classifying preliminary items based on the method of payment.

Classifying Preliminary Items Based on Payment Methods

Understanding how preliminary items are classified based on the method of payment allows us to grasp the financial aspects of these items. Let’s explore the two primary classifications in this context.

1. Single Payment Items: Mobilization Cost

As the name suggests, single-payment items are those that are carried out once and require payment only once. These items do not involve any running costs.

An example of a single payment item is the provision of temporary access roads where maintenance is not required. Once the roads are constructed, the payment is made, and no further financial obligations are associated with these items.

2. Combined Payment Items: Running Cost

Unlike single payment items, combined payment items involve both an initial cost and ongoing monthly expenditures.

Examples of combined payment items include site offices, vehicles for the employer’s and engineer’s use, and telephone connections. These items require an initial investment for their setup or purchase and then incur monthly running costs for their maintenance and operation. Balancing the initial investment with the ongoing expenses is crucial to ensure the smooth functioning of these items throughout the project duration.

With our exploration of preliminary item classifications coming to a close, let’s move forward and address some commonly asked questions related to this topic.

Frequently Asked Questions (FAQs)

- Can preliminaries be allocated to a specific measured work? No, preliminaries are costs that cannot be directly attributed to a specific measured work. They encompass various project-related expenses that support the overall construction operations.

- What happens if a contractor fails to include preliminaries in a BOQ? Failure to include preliminaries in a BOQ can lead to financial and operational complications. These costs are essential for the successful execution of a project and should be properly accounted for to avoid budgetary constraints.

- Are preliminaries fixed throughout the project duration? No, preliminary items can vary in cost and nature. While some items have fixed costs, others may incur running expenses that depend on the project’s duration or specific requirements.

- Do preliminaries differ across construction projects? Yes, preliminaries can vary from one project to another based on the unique requirements, execution strategies, and contractual agreements associated with each project.

- How should preliminary items be documented and managed? Preliminary items should be clearly defined, documented, and accounted for in the project’s BOQ. Proper management and allocation of these costs are crucial for maintaining financial transparency and smooth project operations.

Conclusion

Preliminaries are the hidden heroes that ensure the smooth functioning of construction projects. From contractual requirements to specific needs and execution strategies, these preliminary items play a vital role in laying the foundation for success. By categorizing them based on purpose, cost incurrence, and payment methods, we gain a comprehensive understanding of their significance. So, the next time you embark on a construction project, remember to unlock the power of preliminaries and set the stage for a remarkable achievement.